Featured

Table of Contents

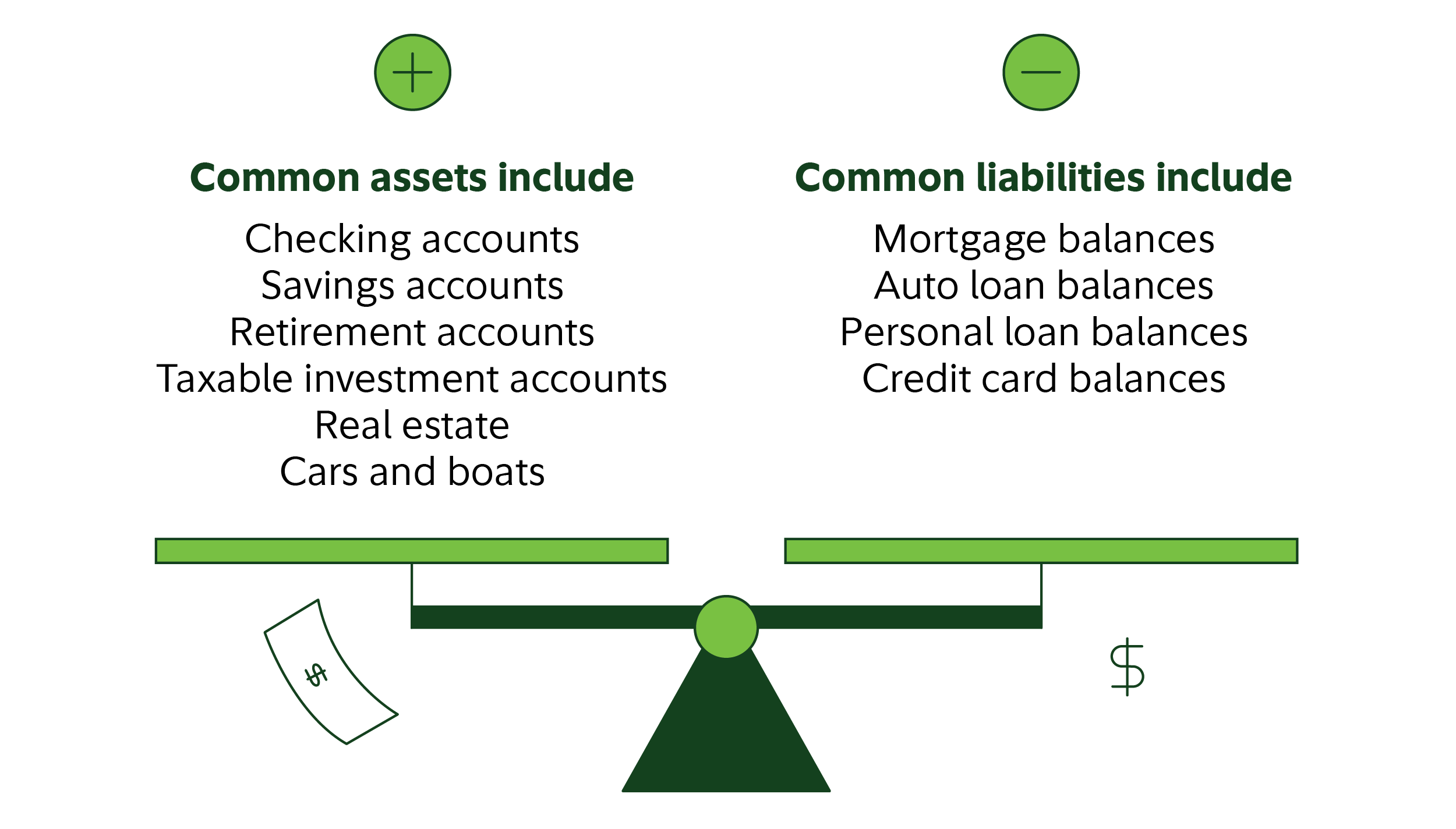

We've compared the leading FinFit options for 2026, consisting of Origin, Bank of America Office Advantages, YNAB, and SmartDollar, with Your Cash Line sticking out as the top option. Unlike product-driven platforms, Your Cash Line delivers a really extensive financial health experience: personalized for each employee, backed by licensed financial coaches, and designed to get rid of the root cause of financial tension, not just manage its signs.

Think about how we approach physical health at work. When an employee gets ill, we don't simply hand them a prescription and send them on their method, we invest in preventive care, yearly examinations, and wellness programs that keep them healthy before a crisis hits.

The emergency situation room costs more than the annual physical. Financial wellness works precisely the same method.

If the underlying cause, no budget plan, no savings routine, no financial roadmap, is never addressed, the next emergency situation is currently on its way. Each short-term repair leaves employees with a little less monetary cushion than previously, making the next crisis more most likely, not less.

They treat the sign. They don't treat the disease. And for HR leaders examining monetary wellness advantages on a tight budget plan and a tight timeline, the "low-cost, low-commitment" appeal of a product-driven platform can be really luring, till you recognize that the cost isn't simply the licensing fee. It's the turnover, the absenteeism, the lost productivity, and the intensifying monetary stress of a workforce that keeps needing the ER due to the fact that nobody ever helped them get healthy in the very first place.

Proven Methods to Improve Your Credit in 2026Guide to HUD-Approved Home Success

They're the yearly physical, not the emergency space., 62.48% of employees state monetary tension has a major or moderate effect on their focus and efficiency at work, and almost seven in ten (68.61%) are actively considering a task change or lowering their work hours as an outcome.

Almost 3 in four (72%) employees state they would likely use financial training or wellness tools if their company offered them. The obstacle is that today's labor force covers several generations with different financial beginning points, various spending pressures, and different levels of monetary literacy. What a per hour employee requires at 25 looks nothing like what a mid-career worker needs at 45.

Its freemium base layer is easy to carry out, and for employees dealing with a real short-term money crisis, the platform's emergency situation credit and loan offerings can seem like a lifeline. However here's what that framing misses: a staff member who requires a loan today and takes one out through FinFit will have less money in their next income.

And the month after that. It's worth keeping in mind that FinFit does provide tools beyond financing, budgeting control panels, financial assessments, and education material are all part of the platform. But in practice, those tools exist along with an organization design constructed around credit and loans, and that tension is difficult to deal with.

Proven Methods to Improve Your Credit in 2026When the company is developed around loaning, the platform prospers when staff members obtain. That's a structural conflict of interest that no quantity of budgeting material or financial education can fully offset.

Are Digital Apps Right for Your Budget?

It's measured in turnover, absenteeism, distracted employees, and health care expenses connected to stress-related disease. An advantage that treats the sign without attending to the origin does not decrease those expenses. It delays them. The question every HR leader should be asking isn't "what does this advantage cost per staff member per year?" It's: "Is this benefit in fact making my workers more solvent, or is it simply making them more comfortable being financially unstable?" Users have noted that linking several bank accounts can be cumbersome, and classifying costs ends up being lengthy to manage.

FinFit does not publicly disclose its rates, and Gartner Peer Insights customers flag a "huge license fee and implementation expense per deal", making it challenging for HR teams to anticipate the real cost before dedicating. The more essential expense isn't the one the employer pays. FinFit's personal loans are released through Celtic Bank, meaning the employer successfully passes the financial problem onto the worker, who is currently struggling.

The platform's freemium label describes the company's cost, not the employee's. Users report that FinFit's series of tools can feel frustrating initially, requiring a considerable ramp-up period before employees feel comfy browsing the platform. A number of have likewise kept in mind a desire for more modification, especially around budgeting classifications to make the experience feel more relevant to their individual financial circumstance.

Strategies to Reduce Household Costs Next Year

Your Cash Line is a coaching-first monetary wellness benefit that integrates licensed human coaches with AI-powered tools to assist employees make better money decisions across every area of their financial life, building the knowledge, confidence, and habits that develop lasting monetary stability. Pros: No loans. No credit lines.

We just win when you do. Origin blends AI-driven tools with access to certified monetary coordinators, covering everything from net-worth tracking and tax planning to investing and estate planning. It tends to be a strong fit for companies with higher-income employees or those browsing more intricate financial circumstances like equity compensation and stock alternatives.

{kind=link}

Latest Posts

Proven Ways to Raise Your FICO Score Fast

Top Rated Wealth Wellness Apps for 2026

Top Performing Wealth Wellness Tools for 2026